Powering India’s shift to electric mobility: Big opportunity in two-wheelers segment

In India, two-wheelers account for 70% of the 200 million plus registered vehicles — contributing to around 20% of the total Carbon Dioxide emissions and about 30% of the particulate emissions in urban areas. The electrification of two-wheelers (2Ws) provides an enormous opportunity to cut down on Carbon Dioxide emissions and improve air quality levels.

As part of the Total Cost of Ownership (TCO) EValuator application, this blog discusses and contrasts the costs of owning and operating electric two-wheelers (e-2Ws) and petrol two-wheelers (petrol-2Ws).

FAME I & II: Government incentives to support e-2Ws

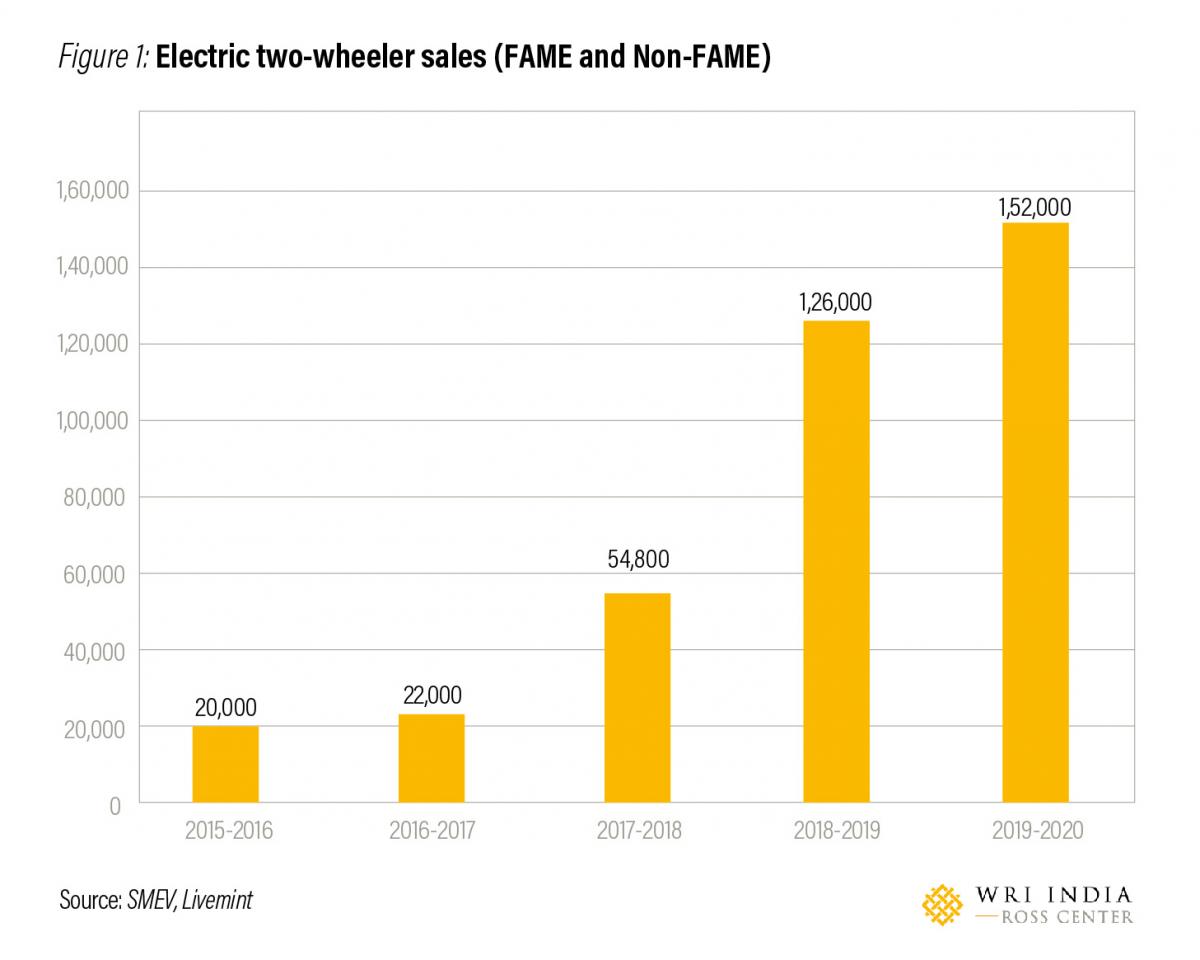

Phase 1 of the Faster Adoption and Manufacturing of (Hybrid &) Electric Vehicles (FAME-I) scheme was launched, in 2015, to accelerate electric vehicle (EV) adoption under the National Electric Mobility Mission Plan 2020. Figure 1 shows the sales of e-2W units in India since 2015, when FAME-I was initiated.

- Around 90% of the vehicles that availed FAME-I incentives were e-2Ws.

- The share of e-2Ws among all 2W sales in FY2020 was approximately 0.6%, which is expected to reach 13% by FY2025.

- Of the e-2Ws sold in FY20, 90% were low-speed scooters (maximum speed of 25 km/hr) because of its lower costs as compared to high-speed and better range e-2W models.

In 2019, the second phase of the FAME scheme (FAME-II) was launched with a total budget outlay of INR 10,000 crore, of which INR 2,000 crore was directed toward providing demand incentives for e-2Ws.

- In FAME-II, the e-2W subsidies are primarily targeted towards high-speed e-2Ws with a minimum range of 80 km per charge, minimum top speed of 40 kmph and powered by advanced battery technology.

- Given the strict guidelines, only 9% of the 152,000 e-2Ws sold in FY20 availed of the FAME-II subsidy.

- However, the market for high-speed e-2Ws is projected to grow by five times, vis-à-vis three-fold growth for low-speed e-2Ws, in the coming five years.

Recently, the Government of India (GOI) has allowed the sale and registration of e-2Ws without factory-fitted batteries to address the issue of high upfront purchase cost of e-2Ws. In addition to the efforts of the GOI, several state governments are also offering various financial and non-financial incentives. For example, the Delhi government is offering up to INR 5,000 per vehicle for scrapping two-wheelers that are not BS-IV certified to encourage petrol-2W owners to upgrade to e-2Ws.

Insights from the WRI India TCO analysis: The economic viability of e-2Ws

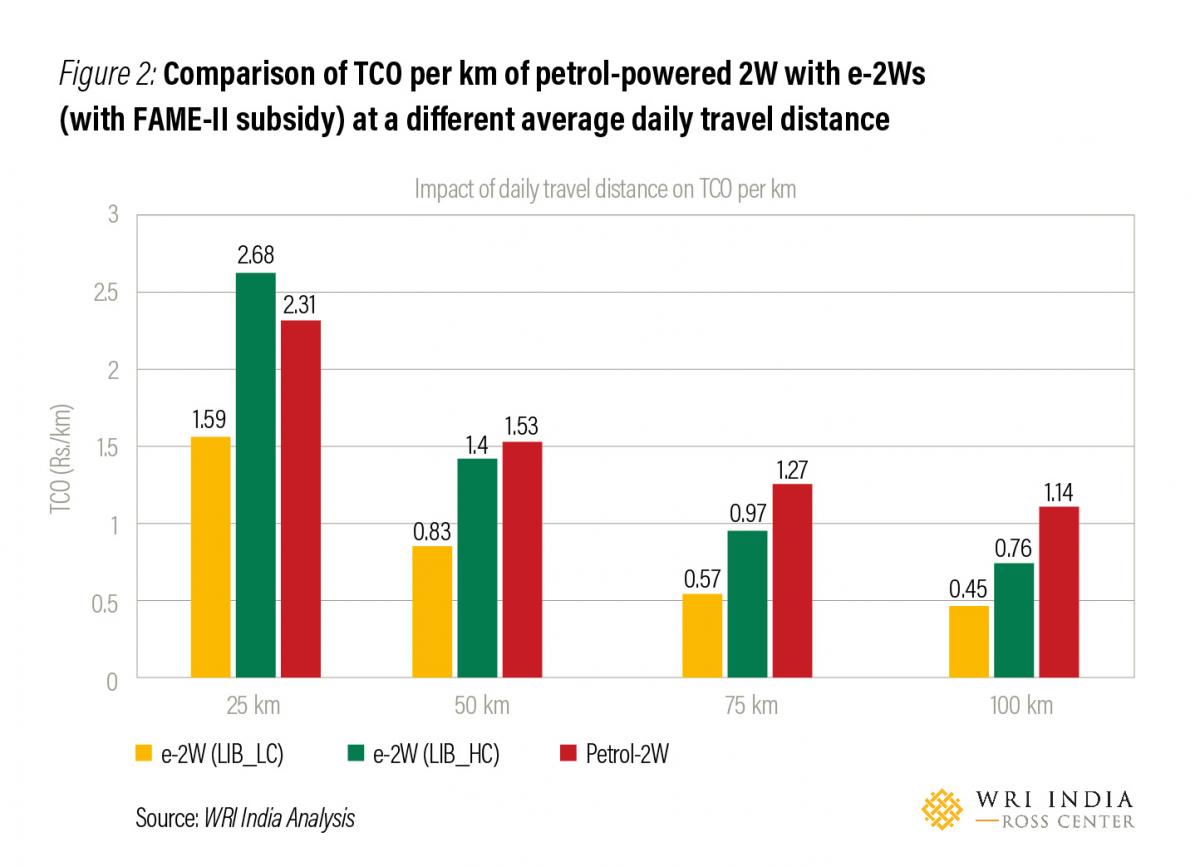

Here, we have compared the TCO per km of lithium-ion low-cost (LIB_LC) and lithium-ion high-cost (LIB_HC) powered e-2Ws with petrol-2W (see Figure 2), at different levels of daily vehicle utilization.

- For private usage, where the typical average daily travel distance is less than 25 km, the TCO per km of low-cost e-2W is less than the high-cost e-2W and petrol-2W.

- For commercial usage, where the typical average daily travel distance is more than 50 km, the TCO per km of both the e-2W variants is less than the petrol-2W.

This indicates that e-2Ws are viable for both private usages as well as commercial applications (last-mile connectivity, last-mile delivery services, etc.) depending on the variant chosen.

Source: WRI India Analysis

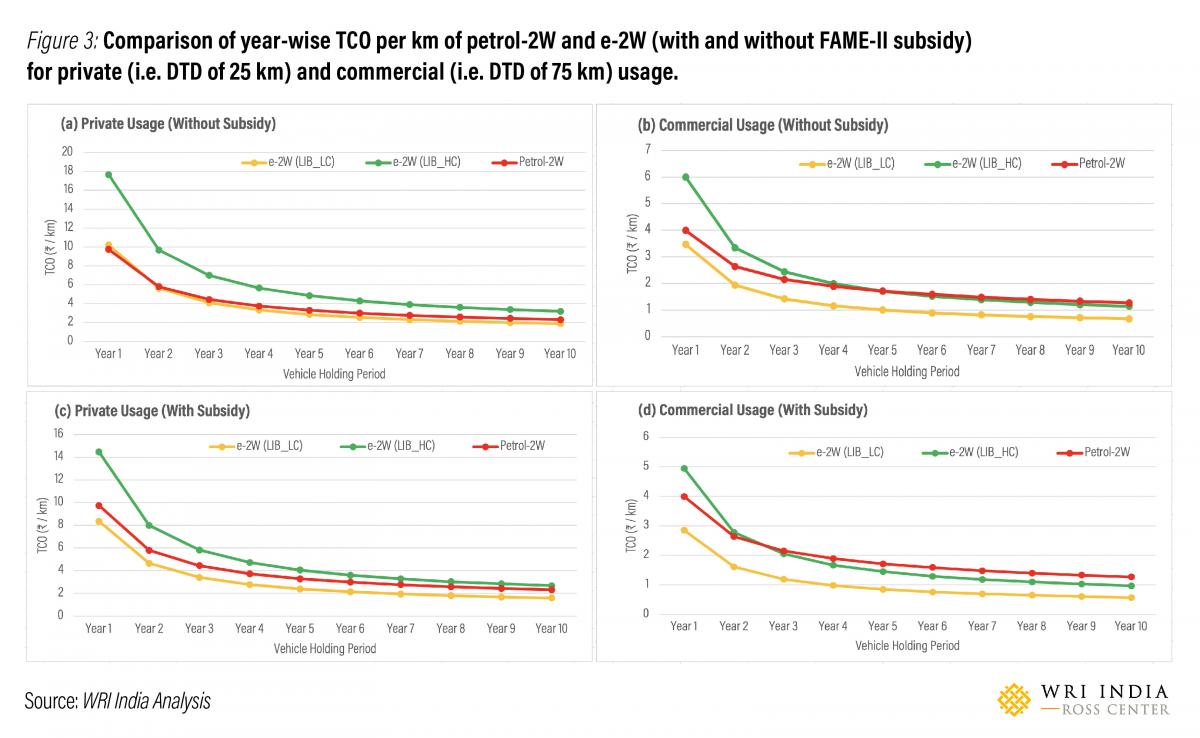

Further, we compare the year-wise TCO to show the effect of the vehicle holding period (the period for which the vehicle is owned) on TCO per km of petrol-2W and e-2Ws, with and without FAME-II subsidy, for private (i.e. Daily Travel Distance (DTD) of 25 km) and commercial (i.e. DTD of 75 km) usage (see Figure 3 (a-d)).

- Without FAME-II subsidy, the TCO per km of the low-cost e-2W becomes cheaper than petrol-2W after third year of ownership on private usage, and from the first year on commercial usage.

- In the case of high-cost e-2W for private usage, the gap in TCO per km with petrol-2W decreases with increasing vehicle holding period, whereas the TCO per km of high-cost e-2W becomes cheaper than petrol-2W after seventh year of ownership on the commercial usage.

- With the FAME-II subsidy factored in, ranging from INR 17,000 to INR 29,000 for the two e-2W variants, the per km TCO of both e-2Ws becomes more competitive as shown.

Emerging business models in the EV industry

The WRI India Ross Center TCO analysis shows that e-2Ws are economically viable, which is borne out by the growing sales in the segment. Commercial segments such as grocery/e-commerce delivery companies and shared mobility services are also rapidly shifting to electric mobility. For example, Flipkart has deployed 30 electric bikes for its last-mile delivery service in Bengaluru while bike-rental company Bounce has 1000 electric scooters in Bengaluru and is collaborating with Ather to expand its electric fleet in Hyderabad. Innovative business models and financing options by e-2W manufacturers are also generating demand for EVs in India –

- Ather Energy is offering a vehicle exchange program and lease options of e-2Ws for a period of 13 to 36 months. Furthermore, Ather also has an option to pay for the battery separately through a monthly subscription model.

- Recently, Ampere Electric has also launched an exchange program, where consumers can exchange petrol-2W for an e-2W.

- Other business strategies include Hero Electric’s three-day trial and promotion scheme, wherein consumers, if unsatisfied, can return the e-2W within three days of purchasing.

Way forward for electric two-wheelers

The Government of India is undertaking several initiatives to achieve 30% electric vehicle (EV) penetration by 2030 with a segmented penetration of 80% for two-wheelers and three-wheelers.

To meet this ambitious target, financial incentives will continue to be required, in the initial years, to encourage uptake. Being a more economically viable EV segment, direct purchase incentives for e-2Ws can be curtailed once adoption reaches a threshold level. Even as industry players intervene through innovative business models to encourage e-2W purchase, central and state governments can offer more on scrappage incentives and other non-financial incentives to further the adoption of e-2Ws.

This is the second blog in a series on TCO analysis of electric vehicles in the Indian market. In the upcoming blogs, we will focus on the findings of the TCO analysis for other vehicle segments as well, to demystify the total costs of owning and operating EVs for individuals and fleet operators, analyze the role of financial incentives and vehicle utilization patterns, and highlight specific implications for policy makers and manufacturers.

Read the previous blog in this series here.

Views expressed here are the author's own.